Any business, irrespective of company size or style, has to accept and process payments from clients. with the variety of payment processing alternatives expanding all the time. It’s more important than ever for business owners to understand all of their access options. The ability of a merchant to receive a transactional payment via a secured channel is referred to as “merchant processing.

- Credit cards are one of the payment methods covered.

- Debit and credit cards

- ACH payments and ACH payments

Payment Terminals in the Cloud

A virtual payment station is an effective solution for internet companies who want to adopt new money-transfer services like credit and debit cards. This type of merchant processing service helps build customer trust in a product or service. While also providing a way for customers to pay for their purchases via a secure channel. Internet solutions that work similarly to POS systems. Provide a secure and convenient way for customers to conduct credit card purchases by just inputting personal information. Consumers can use a virtual payment terminal 24 hours a day, seven days a week, which allows retailers to generate income by accepting payments.

Merchant Services works

Even though merchant-processing services are practically required to be successful in today’s business environment. It is essential to find a dependable and trustworthy provider of these services. Suppliers like Billing tree will provide goods to satisfy the demands of all types of merchants. Simplifying the payments process and improving results for both retailers and their customers.

Most companies take card payments from their consumers, but few people seem to think about it. However, as a company owner, if you don’t understand how to process credit card transactions, you may discover yourself in difficulty when a problem arises. You might even be unsure what a payment processor is. We’ll look at four other payment terms to be aware of the solution to that query.

Cardholders

If you use a debit card (as most of us do), you’re already familiar with the cardholder’s role. But, just to be clear, a cardholder is someone who gets a credit or debit card from a bank that gives out the cards. One can use that card to pay for goods or services at a store.

Merchants

A merchant is a company that sells goods or services. Our explanation, however, is limited to merchants who accept credit cards. That being said, a merchant is any business that has a payment processor that allows them to accept credit or debit cards as payment for goods and services from consumers (cardholders). You are a merchant if you own a company.

Merchant Bank

An acquiring bank is a card organization member (Visa and MasterCard). An acquiring institution is also known as a merchant bank since it works with businesses to establish merchant accounts that allow them to accept credit and debit cards. Accepting banks give merchants the necessary equipment and software to accept cards. Manage customer support and other elements of card acceptance. The acquiring bank also puts money into a company’s account from credit card sales.

Merchant Processing Works

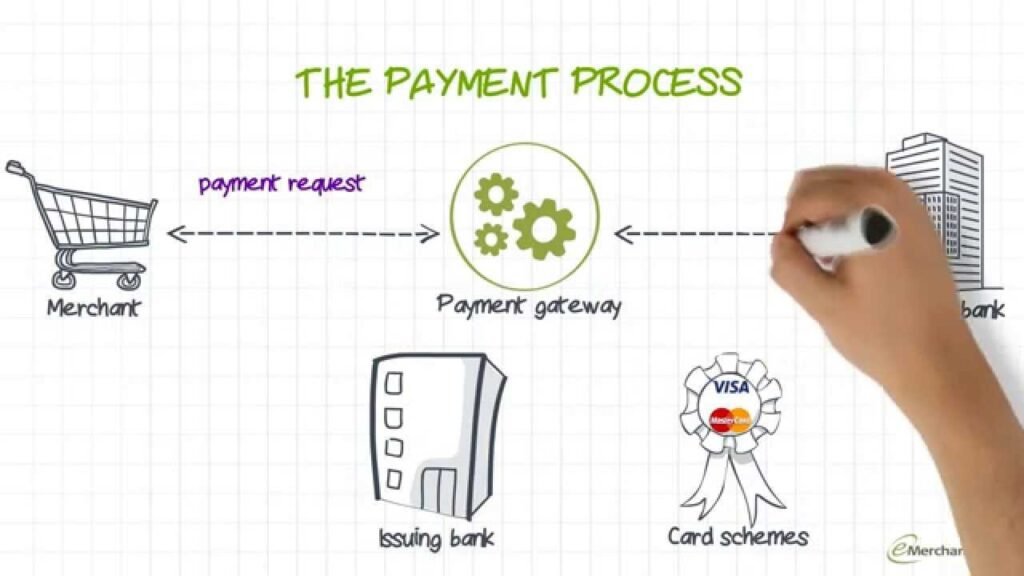

Let’s dive a little deeper into how merchant processing works. Now that you know the players involved, we’ll look at the three main steps for almost every successful card-based transaction: approval, settlement, and funds transfer. While each payment system may have unique processes, these three steps are generally the same.

By understanding each step of the process, merchants can make sure their customers have a smooth and safe experience.

Authorization for Payment

Here’s how authorization works in merchant processing. The merchant’s POS system or online payment tokenizer encrypts payment information before transferring it to the payment gateway when a cardholder swipes, dips, or keys it during the check. Through the card institution’s network, the credit card processor sends this information to the patient’s financial institution.

The badge bank checks to see who the patient is and if he or she has enough money to finish the transaction. From the bank that issued the card to the payment processor to the POS terminal or online payment system of the merchant, the authorization or decline is sent back through the chain. If the transaction is approved, the merchant has completed a legally profitable transaction. However, the funds have not yet been transferred to the merchant’s acquiring bank. This is because the deal requires a second phase of settlement.

Settlement of Funds

Here, payment settlement works with credit cards. The approval is sent to the merchant’s payment processor by the POS terminal or online payment processor. The payment processor then brings the transaction together. The amount of the transaction, less any fees, is put into the merchant’s bank account by the payment processor. Most payments are batched together daily rather than going through the settlement process in real-time. This settlement phase takes either one or two working days. Batching can help merchants save money on total processing expenses if they process hundreds or even thousands of transactions each day.

Before sending the activity balance to the payment processor or acquiring bank, the card networks take the purchase price out of the badge bank. The payment service then puts money in the acquiring bank account of the trader. Before giving the cardholder a bill or statement, the badge bank deducts money (minus fees). The patient’s job ends when they use a debit card. If a person buys something with a credit card, he or she must pay off the account by the next billing cycle to avoid paying interest.

Payment Services for Merchants

A good online payment service will be able to explain its different costs and how they relate to the industry you choose. Keep in mind, however, that merchant accounts depend on your specific case. Most account fees are risk-based based on the type and amount of the company, your credit history, and your previous merchant account history. Always get more information and compare prices to see if factors like this risk will affect you.

Recent Comments